BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

Cerca negli script per "stop loss"

Weekend Hunter Ultimate v6.2 Weekend Hunter Ultimate v6.2 - Automated Crypto Weekend Trading System

OVERVIEW:

Specialized trading strategy designed for cryptocurrency weekend markets (Saturday-Sunday) when institutional traders are typically offline and market dynamics differ significantly from weekdays. Optimized for 15-minute timeframe execution with multi-timeframe confluence analysis.

KEY FEATURES:

- Weekend-Only Trading: Automatically activates during configurable weekend hours

- Dynamic Leverage: 5-20x leverage adjusted based on market safety and signal confidence

- Multi-Timeframe Analysis: Combines 4H trend, 1H momentum, and 15M execution

- 10 Pre-configured Crypto Pairs: BTC, ETH, LINK, XRP, DOGE, SOL, AVAX, PEPE, TON, POL

- Position & Risk Management: Max 4 concurrent positions, -30% account protection

- Smart Trailing Stops: Protects profits when approaching targets

RISK MANAGEMENT:

- Maximum daily loss: 5% (configurable)

- Maximum weekend loss: 15% (configurable)

- Per-position risk: Capped at 120-156 USDT

- Emergency stops for flash crashes (8% moves)

- Consecutive loss protection (4 losses = pause)

TECHNICAL INDICATORS:

- CVD (Cumulative Volume Delta) divergence detection

- ATR-based dynamic stop loss and take profit

- RSI, MACD, Bollinger Bands confluence

- Volume surge confirmation (1.5x average)

- Weekend liquidity adjustments

INTEGRATION:

- Designed for Bybit Futures (0.075% taker fee)

- WunderTrading webhook compatibility via JSON alerts

- Minimum position size: 120 USDT (Bybit requirement)

- Initial capital: $500 recommended

TARGET METRICS:

- Win rate target: 65%

- Average win: 5.5%

- Average loss: 1.8%

- Risk-reward ratio: ~3:1

IMPORTANT DISCLAIMERS:

- Past performance does not guarantee future results

- Leveraged trading carries substantial risk of loss

- Weekend crypto markets have 13% of normal liquidity

- Not suitable for traders who cannot afford to lose their entire investment

- Requires continuous monitoring and adjustment

USAGE:

1. Apply to 15-minute charts only

2. Configure weekend hours for your timezone

3. Set up webhook alerts for automation

4. Monitor performance table in top-right corner

5. Adjust parameters based on your risk tolerance

This is an experimental strategy for educational purposes. Always test with small amounts first and never invest more than you can afford to lose completely.

Rachas ATR AssistHey Traders!

This indicator is a simple, it uses Average True Range (ATR) data from the daily chart and the current timeframe to estimate potential range and volatility.

This indicator compares the daily ATR to the current daily wick range (from low to high), helping you gauge how much "room" might be left for price movement within the day. Alongside that, it shows the ATR over the last 14 candles and 5 candles on your current chart for intraday volatility awareness—ideal for setting stops, targets, or position sizing.

Gauge Daily Potential Movement:

The "Day Range Difference" cell shows how much of the expected daily range (based on ATR) is still unfilled. If the market has moved less than the average, there's still potential for expansion. If it's close to or above the ATR, expect a slowdown or reversal.

Position Sizing & Stop Losses:

Use the 14-period ATR and 5-period ATR on your current timeframe to understand recent volatility. This helps in choosing logical stop loss levels and adjusting position sizes based on market conditions.

Volatility Awareness:

Knowing the average daily range and how much of it has been used lets you avoid entering trades too late in the move or placing stops in overly tight spots.

Table Position & Font:

You can adjust the table location (top/bottom left/right) and font size to best fit your chart layout.

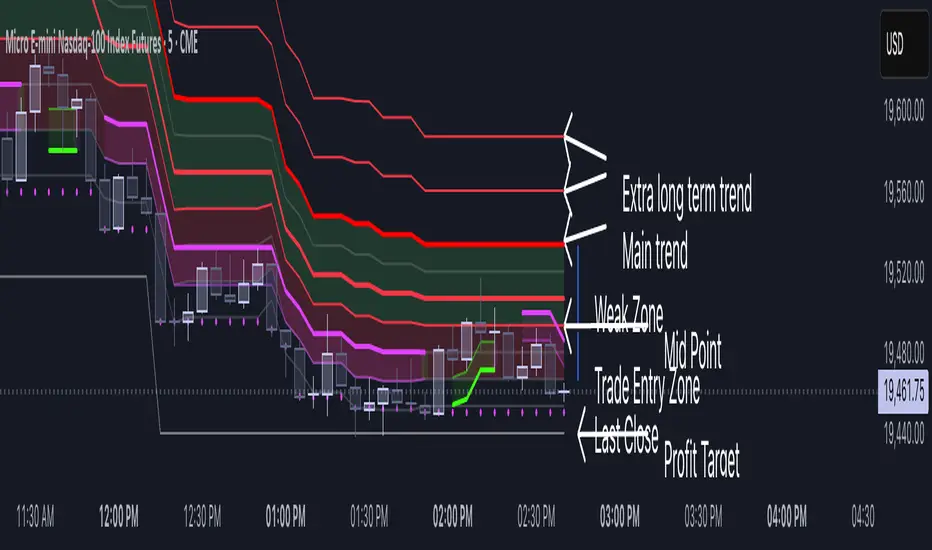

Volatility Layered Supertrend [NLR]We’ve all used Supertrend, but do you know where to actually enter a trade? Volatility Layered Supertrend (VLS) is here to solve that! This advanced trend-following indicator builds on the classic Supertrend by not only identifying trends and their strength but also guiding you to the best trade entry points. VLS divides the main long-term trend into “Strong” and “Weak” Zones, with a clear “Trade Entry Zone” to help you time your trades with precision. With layered trends, dynamic profit targets, and volatility-adaptive bands, VLS delivers actionable signals for any market.

Why I Created VLS Over a Plain Supertrend

I built VLS to address the gaps in traditional Supertrend usage and make trade entries clearer:

Single-Line Supertrend Issues: The default Supertrend sets stop-loss levels that are too wide, making it impractical for most traders to use effectively.

Unclear Entry Points: Standard Supertrend doesn’t tell you where to enter a trade, often leaving you guessing or entering too early or late.

Multi-Line Supertrend Enhancement: Many traders use short, medium, and long Supertrends, which is helpful but can lack focus. In VLS, I include Short, Medium, and Long trends (using multipliers 1 to 3), and add multipliers 4 and 5 to track extra long-term trends—helping to avoid fakeouts that sometimes occur with multiplier 3.

My Solution: I focused on the main long-term Supertrend and split it into “Weak Zone” and “Strength Zone” to show the trend’s reliability. I also defined a “Trade Entry Zone” (starting from the Mid Point, with the first layer’s background hidden for clarity) to guide you on where to enter trades. The zones include Short, Medium, and Long Trend layers for precise entries, exits, and stop-losses.

Practical Trading: This approach provides realistic stop-loss levels, clear entry points, and a “Profit Target” line that aligns with your risk tolerance, while filtering out false signals with longer-term trends.

Key Features

Layered Trend Zones: Short, Medium, Long, and Extra Long Trend layers (up to multipliers 4 and 5) for timing entries and exits.

Strong & Weak Zones: See when the trend is reliable (Strength Zone) or needs caution (Weak Zone).

Trade Entry Zone: A dedicated zone starting from the Mid Point (first layer’s background hidden) to show the best entry points.

Dynamic Profit Targets: A “Profit Target” line that adjusts with the trend for clear goals.

Volatility-Adaptive: Uses ATR to adapt to market conditions, ensuring reliable signals.

Color-Coded: Green for uptrends, red for downtrends—simple and clear.

How It Works

VLS enhances the main long-term Supertrend by dividing it into two zones:

Weak Zone: Indicates a less reliable trend—use tighter stop-losses or wait for the price to reach the Trade Entry Zone.

Strength Zone: Signals a strong trend—ideal for entries with wider stop-losses for bigger moves.

The “Trade Entry Zone” starts at the Mid Point (last layer’s background hidden for clarity), showing you the best area to enter trades. Each zone includes Short, Medium, Long, and Extra Long Trend sublevels (up to multipliers 4 and 5) for precise trade timing and to filter out fakeouts. The “Profit Target” updates dynamically based on trend direction and volatility, giving you a clear goal.

How to Use

Spot the Trend: Green bands = buy, red bands = sell.

Check Strength: Price in Strength Zone? Trend’s reliable—trade confidently. In Weak Zone? Use tighter stops or wait.

Enter Trades: Use the “Trade Entry Zone” (from the Mid Point upward) for the best entry points.

Use Sublevels: Short, Medium, Long, and Extra Long layers in each zone help fine-tune entries and exits.

Set Targets: Follow the Profit Target line for goals—it updates automatically.

Combine Tools: Pair with RSI, MACD, or support/resistance for added confirmation.

Settings

ATR Length: Adjust the ATR period (default 10) to change sensitivity.

Up/Down Colors: Customize colors—green for up, red for down, by default.

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

Heiken Ashi Supertrend ATR-SL StrategyThis indicator combines Heikin Ashi candle pattern analysis with Supertrend to generate high-probability trading signals with built-in risk management. It identifies potential entries and exits based on specific Heikin Ashi candlestick formations while providing automated ATR-based stop loss management.

Trading Logic:

The system generates long signals when a green Heikin Ashi candle forms with no bottom wick (indicating strong bullish momentum). Short signals appear when a red Heikin Ashi candle forms with no top wick (showing strong bearish momentum). The absence of wicks on these candles signals a high-conviction market move in the respective direction.

Exit signals are triggered when:

1. An opposite pattern forms (red candle with no top wick exits longs; green candle with no bottom wick exits shorts)

2. The ATR-based stop loss is hit

3. The break-even stop is activated and then hit

Technical Approach:

- Select Heiken Ashi Canldes on your Trading View chart. Entried are based on HA prices.

- Supertrend and ATR-based stop losses use real price data (not HA values) for trend determination

- ATR-based stop losses automatically adjust to market volatility

- Break-even functionality moves the stop to entry price once price moves a specified ATR multiple in your favor

Risk Management:

- Default starting capital: 1000 units

- Default risk per trade: 10% of equity (customizable in strategy settings)

- Hard Stop Loss: Set ATR multiplier (default: 2.0) for automatic stop placement

- Break Even: Configure ATR threshold (default: 1.0) to activate break-even stops

- Appropriate position sizing relative to equity and stop distance

Customization Options:

- Supertrend Settings:

- Enable/disable Supertrend filtering (trade only in confirmed trend direction)

- Adjust Factor (default: 3.0) to change sensitivity

- Modify ATR Period (default: 10) to adapt to different timeframes

Visual Elements:

- Green triangles for long entries, blue triangles for short entries

- X-marks for exits and stop loss hits

- Color-coded position background (green for long, blue for short)

- Clearly visible stop loss lines (red for hard stop, white for break-even)

- Comprehensive position information label with entry price and stop details

Implementation Notes:

The indicator tracks positions internally and maintains state across bars to properly manage stop levels. All calculations use confirmed bars only, with no repainting or lookahead bias. The system is designed for swing trading on timeframes from 1-hour and above, where Heikin Ashi patterns tend to be more reliable.

This indicator is best suited for traders looking to combine the pattern recognition strengths of Heikin Ashi candles with the trend-following capabilities of Supertrend, all while maintaining disciplined risk management through automated stops.

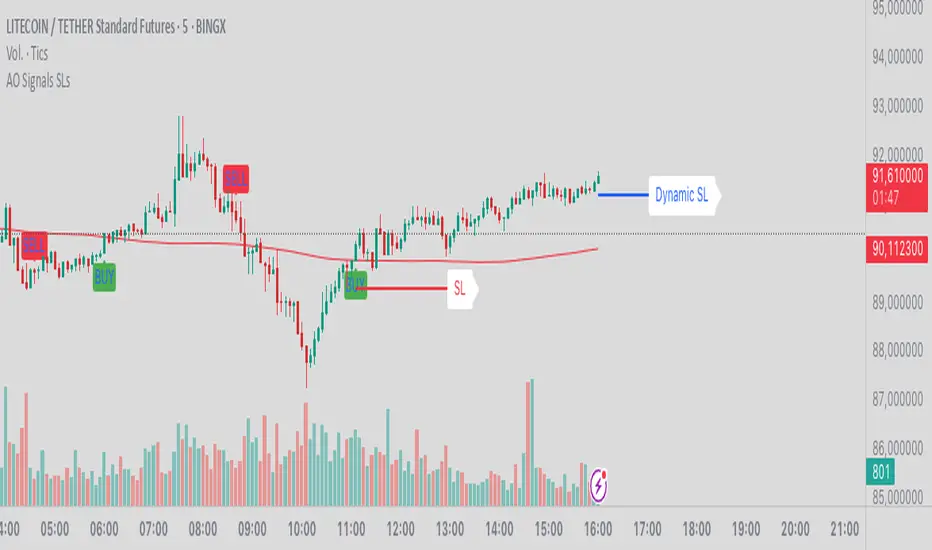

AO Smart Scalper – 5M Dynamic SL Edition📈 AO Signals with Fixed and Dynamic SL – Optimized for 5-Minute Charts 📉

This indicator is built for 5-minute timeframe trading, combining powerful momentum signals from the Awesome Oscillator (AO) with both Fixed and Dynamic Stop Loss (SL) levels to enhance trade management and risk control.

✅ Buy/Sell Signals:

The indicator generates clear BUY and SELL signals based on the AO crossing above or below the zero line, helping traders capture momentum shifts early.

🛑 Fixed Stop Loss:

Each trade signal comes with a Fixed SL, calculated based on the high (for shorts) or low (for longs) of the previous candle, with a customizable percentage offset. This SL is plotted with a red line, providing a clear initial risk level.

⚡ Dynamic Stop Loss: Continuous Presence, Strategic Use:

A secondary Dynamic SL line is plotted, which is continuously present on the chart. This dynamic level responds to market conditions and can serve as a trailing stop or key decision point.

💡 Recommended Use: It is recommended to actively start using the Dynamic SL once the trade has moved into profit. This allows protecting obtained profits and minimizing the risk of losses in case of a market reversal.

🛡️ Enhanced Dynamic Stop-Loss Strategy:

🔒 Initial Protection: Utilize the Fixed SL as the initial stop-loss, placed below relevant lows (for longs) or above relevant highs (for shorts), or as provided by the fixed SL indicator.

🛤️ Dynamic Tracking:

🟢 Long Trades: Once in profit, the Dynamic SL will dynamically adjust, moving upwards as higher lows are formed, effectively trailing the price and securing profits.

🔴 Short Trades: Conversely, in short trades, once in profit, the Dynamic SL will move downwards as lower highs are formed, protecting gains.

🔄 Alternatively the dynamic stop loss will follow the dynamic SL line provided by the indicator.

🚪 Exiting Trades: When the price crosses below the Dynamic SL line in a LONG trade, or above it in a SHORT trade, the recommended action is to exit the trade.

↩️ Re-entry Consideration: You may consider re-entering only if the price clearly returns above the Dynamic SL (for longs) or below it (for shorts).

⚠️ IMPORTANT - 5-Minute Strategy Guidance ⏱️

This tool is specifically optimized for the 5-minute timeframe. This approach helps filter out weak setups and maintain discipline in volatile market conditions.

✨ Additional Features:

👁️ Visual and editable SL levels

📊 200-period SMA for trend context

💻 Simple and effective interface for intraday trading setups

🎯 Ideal for traders seeking a clean, rule-based system that combines momentum entry signals with layered stop loss protection.

🔑 Key Changes:

It was emphasized that the Dynamic SL is always present, but its active use is recommended once the trade is in profit.

It was clarified the use of the Fixed SL, giving the option to use the one provided by the indicator, or to place it according to the price action.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

Smart MA Crossover BacktesterSmart MA Crossover Backtester - Strategy Overview

Strategy Name: Smart MA Crossover Backtester

Published on: TradingView

Applicable Markets: Works well on crypto (tested profitably on ETH)

Strategy Concept

The Smart MA Crossover Backtester is an improved Moving Average (MA) crossover strategy that incorporates a trend filter and an ATR-based stop loss & take profit mechanism for better risk management. It aims to capture trends efficiently while reducing false signals by only trading in the direction of the long-term trend.

Core Components & Logic

Moving Averages (MA) for Entry Signals

Fast Moving Average (9-period SMA)

Slow Moving Average (21-period SMA)

A trade signal is generated when the fast MA crosses the slow MA.

Trend Filter (200-period SMA)

Only enters long positions if price is above the 200-period SMA (bullish trend).

Only enters short positions if price is below the 200-period SMA (bearish trend).

This helps in avoiding counter-trend trades, reducing whipsaws.

ATR-Based Stop Loss & Take Profit

Uses the Average True Range (ATR) with a multiplier of 2 to calculate stop loss.

Risk-Reward Ratio = 1:2 (Take profit is set at 2x ATR).

This ensures dynamic stop loss and take profit levels based on market volatility.

Trading Rules

✅ Long Entry (Buy Signal):

Fast MA (9) crosses above Slow MA (21)

Price is above the 200 MA (bullish trend filter active)

Stop Loss: Below entry price by 2× ATR

Take Profit: Above entry price by 4× ATR

✅ Short Entry (Sell Signal):

Fast MA (9) crosses below Slow MA (21)

Price is below the 200 MA (bearish trend filter active)

Stop Loss: Above entry price by 2× ATR

Take Profit: Below entry price by 4× ATR

Why This Strategy Works Well for Crypto (ETH)?

🔹 Crypto markets are highly volatile – ATR-based stop loss adapts dynamically to market conditions.

🔹 Long-term trend filter (200 MA) ensures trading in the dominant direction, reducing false signals.

🔹 Risk-reward ratio of 1:2 allows for profitable trades even with a lower win rate.

This strategy has been tested on Ethereum (ETH) and has shown profitable performance, making it a strong choice for crypto traders looking for trend-following setups with solid risk management. 🚀

Dual Strategy Selector V2 - CryptogyaniOverview:

This script provides traders with a dual-strategy system that they can toggle between using a simple dropdown menu in the input settings. It is designed to cater to different trading styles and needs, offering both simplicity and advanced filtering techniques. The strategies are built around moving average crossovers, enhanced by configurable risk management tools like take profit levels, trailing stops, and ATR-based stop-loss.

Key Features:

Two Strategies in One Script:

Strategy 1: A classic moving average crossover strategy for identifying entry signals based on trend reversals. Includes user-defined take profit and trailing stop-loss options for profit locking.

Strategy 2: An advanced trend-following system that incorporates:

A higher timeframe trend filter to confirm entry signals.

ATR-based stop-loss for dynamic risk management.

Configurable partial take profit to secure gains while letting the trade run.

Highly Customizable:

All key parameters such as SMA lengths, take profit levels, ATR multiplier, and timeframe for the trend filter are adjustable via the input settings.

Dynamic Toggle:

Traders can switch between Strategy 1 and Strategy 2 with a single dropdown, allowing them to adapt the strategy to market conditions.

How It Works:

Strategy 1:

Entry Logic: A long trade is triggered when the fast SMA crosses above the slow SMA.

Exit Logic: The trade exits at either a user-defined take profit level (percentage or pips) or via an optional trailing stop that dynamically adjusts based on price movement.

Strategy 2:

Entry Logic: Builds on the SMA crossover logic but adds a higher timeframe trend filter to align trades with the broader market direction.

Risk Management:

ATR-Based Stop-Loss: Protects against adverse moves with a volatility-adjusted stop-loss.

Partial Take Profit: Allows traders to secure a percentage of gains while keeping some exposure for extended trends.

How to Use:

Select Your Strategy:

Use the dropdown in the input settings to choose Strategy 1 or Strategy 2.

Configure Parameters:

Adjust SMA lengths, take profit, and risk management settings to align with your trading style.

For Strategy 2, specify the higher timeframe for trend filtering.

Deploy and Monitor:

Apply the script to your preferred asset and timeframe.

Use the backtest results to fine-tune settings for optimal performance.

Why Choose This Script?:

This script stands out due to its dual-strategy flexibility and enhanced features:

For beginners: Strategy 1 provides a simple yet effective trend-following system with minimal setup.

For advanced traders: Strategy 2 includes powerful tools like trend filters and ATR-based stop-loss, making it ideal for challenging market conditions.

By combining simplicity with advanced features, this script offers something for everyone while maintaining full transparency and user customization.

Default Settings:

Strategy 1:

Fast SMA: 21, Slow SMA: 49

Take Profit: 7% or 50 pips

Trailing Stop: Optional (disabled by default)

Strategy 2:

Fast SMA: 20, Slow SMA: 50

ATR Multiplier: 1.5

Partial Take Profit: 50%

Higher Timeframe: 1 Day (1D)

Triple EMA Crossover StrategyTriple EMA Crossover Strategy

Overview

The Triple EMA Crossover Strategy is a trend-following trading system that utilizes three Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. This strategy is based on the principle that when shorter-term prices cross above longer-term prices, it can indicate a bullish trend, and conversely when they cross below, it can signal a bearish trend.

Components

Exponential Moving Averages (EMAs):

Short EMA: A fast-moving average that reacts quickly to price changes (commonly set to 9 periods).

Medium EMA: A medium-term average that smooths out price data and helps confirm trends (commonly set to 21 periods).

Long EMA: A slow-moving average that helps identify the overall trend direction (commonly set to 55 periods).

Trading Signals:

Buy Signal: A long entry is triggered when:

The Short EMA (9) crosses above the Medium EMA (21).

The Medium EMA (21) is above the Long EMA (55).

Sell Signal: A short entry is signaled when:

The Short EMA (9) crosses below the Medium EMA (21).

The Medium EMA (21) is below the Long EMA (55).

Stop Loss and Take Profit:

Stop Loss: Implement a predefined percentage or ATR-based stop loss to limit potential losses.

Take Profit: Set a target based on a risk-to-reward ratio that reflects your trading strategy's goals.

Advantages

Trend Identification: The EMA crossover system allows traders to identify the current trend dynamically, focusing on upward or downward price movements.

Simplicity: The strategy is straightforward, making it accessible for both new and experienced traders.

Flexibility: This method can be applied across multiple timeframes and asset classes, making it versatile for various trading styles.

Disadvantages

Lagging Indicator: Moving averages are lagging indicators, meaning signals may come later than the actual price movement, which can lead to missed opportunities.

Whipsaw Effect: In ranging markets, the strategy may produce false signals leading to potential losses.

ETH Signal 15m

This strategy uses the Supertrend indicator combined with RSI to generate buy and sell signals, with stop loss (SL) and take profit (TP) conditions based on ATR (Average True Range). Below is a detailed explanation of each part:

1. General Information BINANCE:ETHUSDT.P

Strategy Name: "ETH Signal 15m"

Designed for use on the 15-minute time frame for the ETH pair.

Default capital allocation is 15% of total equity for each trade.

2. Backtest Period

start_time and end_time: Define the start and end time of the backtest period.

start_time = 2024-08-01: Start date of the backtest.

end_time = 2054-01-01: End date of the backtest.

The strategy will only run when the current time falls within this specified range.

3. Supertrend Indicator

Supertrend is a trend-following indicator that provides buy or sell signals based on the direction of price changes.

factor = 2.76: The multiplier used in the Supertrend calculation (increasing this value makes the Supertrend less sensitive to price movements).

atrPeriod = 12: Number of periods used to calculate ATR.

Output:

direction: Determines the buy/sell direction based on Supertrend.

If direction decreases, it signals a buy (Long).

If direction increases, it signals a sell (Short).

4. RSI Indicator

RSI (Relative Strength Index) is a momentum indicator, often used to identify overbought or oversold conditions.

rsiLength = 12: Number of periods used to calculate RSI.

rsiOverbought = 70: RSI level considered overbought.

rsiOversold = 30: RSI level considered oversold.

5. Entry Conditions

Long Entry:

Supertrend gives a buy signal (ta.change(direction) < 0).

RSI must be below the overbought level (rsi < rsiOverbought).

Short Entry:

Supertrend gives a sell signal (ta.change(direction) > 0).

RSI must be above the oversold level (rsi > rsiOversold).

The strategy will only execute trades if the current time is within the backtest period (in_date_range).

6. Stop Loss (SL) and Take Profit (TP) Conditions

ATR (Average True Range) is used to calculate the distance for Stop Loss and Take Profit based on price volatility.

atr = ta.atr(atrPeriod): ATR is calculated using 12 periods.

Stop Loss and Take Profit are calculated as follows:

Long Trade:

Stop Loss: Set at close - 4 * atr (current price minus 4 times the ATR).

Take Profit: Set at close + 2 * atr (current price plus 2 times the ATR).

Short Trade:

Stop Loss: Set at close + 4 * atr (current price plus 4 times the ATR).

Take Profit: Set at close - 2.237 * atr (current price minus 2.237 times the ATR).

Summary:

This strategy enters a Long trade when the Supertrend indicates an upward trend and RSI is not in the overbought region. Conversely, a Short trade is entered when Supertrend signals a downtrend, and RSI is not oversold.

The trade is exited when the price reaches the Stop Loss or Take Profit levels, which are determined based on price volatility (ATR).

Disclaimer:

The content provided in this strategy is for informational and educational purposes only. It is not intended as financial, investment, or trading advice. Trading in cryptocurrency, stocks, or any financial markets involves significant risk, and you may lose more than your initial investment. Past performance is not indicative of future results, and no guarantee of profit can be made. You should consult with a professional financial advisor before making any investment decisions. The creator of this strategy is not responsible for any financial losses or damages incurred as a result of following this strategy. All trades are executed at your own risk.

Fractal Breakout Trend Following StrategyOverview

The Fractal Breakout Trend Following Strategy is a trend-following system which utilizes the Willams Fractals and Alligator to execute the long trades on the fractal's breakouts which have a high probability to be the new uptrend phase beginning. This system also uses the normalized Average True Range indicator to filter trades after a large moves, because it's more likely to see the trend continuation after a consolidation period. Strategy can execute only long trades.

Unique Features

Trend and volatility filtering system: Strategy uses Williams Alligator to filter the counter-trend fractals breakouts and normalized Average True Range to avoid the trades after large moves, when volatility is high

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Flexible Risk Management: Users can choose the stop-loss percent (by default = 3%) for trades, but strategy also has the dynamic stop-loss level using down fractals.

Methodology

The strategy places stop order at the last valid fractal breakout level. Validity of this fractal is defined by the Williams Alligator indicator. If at the moment of time when price breaking the last fractal price is higher than Alligator's teeth line (8 period SMA shifted 5 bars in the future) this is a valid breakout. Moreover strategy has the additional volatility filtering system using normalized ATR. It calculates the average normalized ATR for last user-defined number of bars and if this value lower than the user-defined threshold value the long trade is executed.

When trade is opened, script places the stop loss at the price higher of two levels: user defined stop-loss from the position entry price or down fractal validation level. The down fractal is valid with the rule, opposite as the up fractal validation. Price shall break to the downside the last down fractal below the Willians Alligator's teeth line.

Strategy has no fixed take profit. Exit level changes with the down fractal validation level. If price is in strong uptrend trade is going to be active until last down fractal is not valid. Strategy closes trade when price hits the down fractal validation level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 3% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Williams Fractals to open long trade when price has broken the key resistance level to the upside. This resistance level is the last up fractal and is shall be broken above the Williams Alligator's teeth line to be qualified as the valid breakout according to this strategy. The Alligator filtering increases the probability to avoid the false breakouts against the current trend.

Moreover strategy has an additional filter using Average True Range(ATR) indicator. If average value of ATR for the last user-defined number of bars is lower than user-defined threshold strategy can open the long trade according to open trade condition above. The logic here is following: we want to open trades after period of price consolidation inside the range because before and after a big move price is more likely to be in sideways, but we need a trend move to have a profit.

Another one important feature is how the exit condition is defined. On the one hand, strategy has the user-defined stop-loss (3% below the entry price by default). It's made to give users the opportunity to restrict their losses according to their risk-tolerance. On the other hand, strategy utilizes the dynamic exit level which is defined by down fractal activation. If we assume the breaking up fractal is the beginning of the uptrend, breaking down fractal can be the start of downtrend phase. We don't want to be in long trade if there is a high probability of reversal to the downside. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.19%

Maximum Single Profit: +24.97%

Net Profit: +3036.90 USDT (+30.37%)

Total Trades: 83 (28.92% win rate)

Profit Factor: 1.953

Maximum Accumulated Loss: 963.98 USDT (-8.29%)

Average Profit per Trade: 36.59 USDT (+1.12%)

Average Trade Duration: 72 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h and higher time frames and the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

SR EMA ORBSR EMA ORB combines your Support/Resistance pivot levels + EMA crossover labels/alerts with an optional Opening Range Breakout (ORB) module that can work on higher timeframes using LTF calculation (via request.security).

What it shows

1) Support/Resistance (Pivot based)

Plots pivot Resistance (red) and Support (blue).

Optional break labels:

B for break with volume confirmation (Volume Osc > Threshold)

Bull Wick / Bear Wick wick-based breaks

2) EMA Crossovers (visual + alerts)

Labels:

Up (ST EMA crosses above MT EMA)

Down (ST EMA crosses below MT EMA)

Buy (MT EMA crosses above LT EMA)

Sell (MT EMA crosses below LT EMA)

Includes the original alert() messages exactly like your Script 1.

3) ORB (Opening Range Breakout)

Builds an opening range for the configured “ORB Window” (default: 10 minutes).

After the window ends, it waits for a breakout:

Breakout based on Close or EMA

Optional breakout buffer %

Optional volume filter (uses your Volume Threshold logic)

Entry requires retests based on sensitivity:

High = 0 retests

Medium = 1 retest

Low = 2 retests

Lowest = 3 retests

Shows:

ORB High / ORB Low lines (unique colors, bold width)

ORB Entry label (ORB)

Optional TP1/SL markers (if enabled)

4) Confluence (optional confidence marker)

Prints a separate CONF label when:

ORB entry happens AND

EMA direction agrees (rule selectable)

Optional: also require SR break in the same direction

5) RR helper (optional)

Draws Entry / SL / TP target lines at 1:2 or 1:3

Trigger can be:

ORB Entry

Confluence only (recommended)

6) Dashboards (optional)

Compact ORB dashboard: current bias + entry + SL

Backtest dashboard: trades, wins, losses, win%

Timeframe behavior (important)

ORB supports these window selections: 1m, 5m, 10m, 15m, 30m, 1h, 1D, 1W, 1M

ORB supports these calc TF selections: 1m, 3m, 5m, 10m, 15m, 30m, 1h

Mode

Auto: uses Native when chart TF is supported, otherwise switches to LTF calculation

Native: ORB runs only on supported chart TF; disables otherwise

LTF: ORB always calculates on Calc TF (best for 1H/1D chart viewing)

Examples (recommended setups)

Example 1 — Your main setup (10m ORB on intraday chart)

Goal: trade ORB normally with minimal complexity

Chart TF: 1m / 3m / 5m

ORB:

Mode: Auto

ORB Window: 10m

Calc TF: 10m (or 5m if you want slightly earlier structure)

Sensitivity: Medium

Breakout Condition: Close

TP Method: Dynamic

Stop Loss: Balanced

Visuals:

Draw ORB Lines: ON

Entry Labels: ON

TP/SL Marks: OFF (keeps chart clean)

Example 2 — View ORB on a 1H chart (LTF-on-HTF mode)

Goal: see 10m ORB levels/signals while looking at 1H structure

Chart TF: 1H

ORB:

Mode: LTF

ORB Window: 10m

Calc TF: 5m or 10m

Sensitivity: Medium

Note: On HTF, multiple LTF events can compress into fewer visible updates (normal with security data).

Example 3 — Higher winrate attempt (fewer trades, more filtering)

Goal: reduce bad ORB entries

ORB:

Sensitivity: Low (2 retests)

Breakout Buffer %: 0.10 – 0.25

Use Vol Osc Filter: ON

Educational Use Only: This script is provided for educational and informational purposes only and is not financial advice—use it at your own risk, as trading involves substantial risk of loss.

Confluence:

Enable Confluence: ON

EMA Rule: Stack (strict)

Require SR Break Same Direction: ON (optional, strict)

RR:

RR Lines: ON

RR: 1:3

Trigger: Confluence

This usually reduces signals but can improve quality depending on ticker.

Example 4 — Conservative risk control (visual RR planning)

Goal: only take trades that offer clear RR

RR:

Show RR Lines: ON

RR: 1:2

Trigger: Confluence

Result: you only see RR targets when the entry is “higher confidence”.

Example 5 — Dashboards only when needed

Goal: keep chart clean, but enable quick stats occasionally

ORB UI:

Show ORB Dashboard: OFF normally

Show Backtest Dashboard: ON only during tuning

Positions: set to Top Right / Top Center as you prefer

Notes on alerts (how to use)

Your SR/EMA alerts are built-in alert() calls, so when creating an alert choose:

“Any alert() function call”

ORB/CONF alerts are alertcondition(), so create alerts selecting:

ORB Entry

ORB TP1

ORB SL

CONF Buy / CONF Sell

Support Resistance EMA Crossovers with ORB and AlertsSR EMA ORB combines your Support/Resistance pivot levels + EMA crossover labels/alerts with an optional Opening Range Breakout (ORB) module that can work on higher timeframes using LTF calculation (via request.security).

What it shows

1) Support/Resistance (Pivot based)

Plots pivot Resistance (red) and Support (blue).

Optional break labels:

B for break with volume confirmation (Volume Osc > Threshold)

Bull Wick / Bear Wick wick-based breaks

2) EMA Crossovers (visual + alerts)

Labels:

Up (ST EMA crosses above MT EMA)

Down (ST EMA crosses below MT EMA)

Buy (MT EMA crosses above LT EMA)

Sell (MT EMA crosses below LT EMA)

Includes the original alert() messages exactly like your Script 1.

3) ORB (Opening Range Breakout)

Builds an opening range for the configured “ORB Window” (default: 10 minutes).

After the window ends, it waits for a breakout:

Breakout based on Close or EMA

Optional breakout buffer %

Optional volume filter (uses your Volume Threshold logic)

Entry requires retests based on sensitivity:

High = 0 retests

Medium = 1 retest

Low = 2 retests

Lowest = 3 retests

Shows:

ORB High / ORB Low lines (unique colors, bold width)

ORB Entry label (ORB)

Optional TP1/SL markers (if enabled)

4) Confluence (optional confidence marker)

Prints a separate CONF label when:

ORB entry happens AND

EMA direction agrees (rule selectable)

Optional: also require SR break in the same direction

5) RR helper (optional)

Draws Entry / SL / TP target lines at 1:2 or 1:3

Trigger can be:

ORB Entry

Confluence only (recommended)

6) Dashboards (optional)

Compact ORB dashboard: current bias + entry + SL

Backtest dashboard: trades, wins, losses, win%

Timeframe behavior (important)

ORB supports these window selections: 1m, 5m, 10m, 15m, 30m, 1h, 1D, 1W, 1M

ORB supports these calc TF selections: 1m, 3m, 5m, 10m, 15m, 30m, 1h

Mode

Auto: uses Native when chart TF is supported, otherwise switches to LTF calculation

Native: ORB runs only on supported chart TF; disables otherwise

LTF: ORB always calculates on Calc TF (best for 1H/1D chart viewing)

Examples (recommended setups)

Example 1 — Your main setup (10m ORB on intraday chart)

Goal: trade ORB normally with minimal complexity

Chart TF: 1m / 3m / 5m

ORB:

Mode: Auto

ORB Window: 10m

Calc TF: 10m (or 5m if you want slightly earlier structure)

Sensitivity: Medium

Breakout Condition: Close

TP Method: Dynamic

Stop Loss: Balanced

Visuals:

Draw ORB Lines: ON

Entry Labels: ON

TP/SL Marks: OFF (keeps chart clean)

Example 2 — View ORB on a 1H chart (LTF-on-HTF mode)

Goal: see 10m ORB levels/signals while looking at 1H structure

Chart TF: 1H

ORB:

Mode: LTF

ORB Window: 10m

Calc TF: 5m or 10m

Sensitivity: Medium

Note: On HTF, multiple LTF events can compress into fewer visible updates (normal with security data).

Example 3 — Higher winrate attempt (fewer trades, more filtering)

Goal: reduce bad ORB entries

ORB:

Sensitivity: Low (2 retests)

Breakout Buffer %: 0.10 – 0.25

Use Vol Osc Filter: ON

Confluence:

Enable Confluence: ON

EMA Rule: Stack (strict)

Require SR Break Same Direction: ON (optional, strict)

RR:

RR Lines: ON

RR: 1:3

Trigger: Confluence

This usually reduces signals but can improve quality depending on ticker.

Example 4 — Conservative risk control (visual RR planning)

Goal: only take trades that offer clear RR

RR:

Show RR Lines: ON

RR: 1:2

Trigger: Confluence

Result: you only see RR targets when the entry is “higher confidence”.

Example 5 — Dashboards only when needed

Goal: keep chart clean, but enable quick stats occasionally

ORB UI:

Show ORB Dashboard: OFF normally

Show Backtest Dashboard: ON only during tuning

Positions: set to Top Right / Top Center as you prefer

Notes on alerts (how to use)

Your SR/EMA alerts are built-in alert() calls, so when creating an alert choose:

“Any alert() function call”

ORB/CONF alerts are alertcondition(), so create alerts selecting:

ORB Entry

ORB TP1

ORB SL

CONF Buy / CONF Sell

Educational Use Only: This script is provided for educational and informational purposes only and is not financial advice—use it at your own risk, as trading involves substantial risk of loss.

Liquidity Trap Strategy - ATR OptimizedLiquidity Trap Strategy – Optimized Version

1. Overview

The Liquidity Trap Strategy is a high-probability price action trading system designed to exploit “trapped buyers or sellers” around key levels from the previous trading day.

Markets: Works on any market (Forex, Crypto, Futures, Indices, Stocks)

Timeframes: Designed for 15-minute (15m) and 1-hour (1H) charts

Trading Style: “Hunter” style — trades may not happen every day, but setups are high-probability

Trade Frequency: Only first trade per day is taken for simplicity and high quality

2. Key Components

a) Daily Levels

Previous Day High (PDH) and Previous Day Low (PDL) are automatically calculated using the prior day’s bar.

These are drawn as anchored horizontal lines, extending to the current day.

PDH/PDL act as key support/resistance zones — areas where liquidity is often trapped.

b) Trap Concept

The strategy is based on the “liquidity trap” principle:

Buyer Trap (Short Entry):

Price breaks above the previous day high (PDH) → buyers think price will continue higher.

Price reverses immediately below PDH, trapping aggressive buyers above the key level.

This creates selling pressure, giving an opportunity to enter short.

Seller Trap (Long Entry):

Price breaks below the previous day low (PDL) → sellers think price will continue lower.

Price reverses immediately above PDL, trapping aggressive sellers below the key level.

This creates buying pressure, giving an opportunity to enter long.

The key idea: trapped traders cause the market to move in the opposite direction of the breakout, creating high-probability moves.

c) Trade Execution Logic

Buyer Trap / Short Entry:

Condition: high > PDH AND close < PDH AND no trade taken yet today

Entry: Short at the close of the trap candle

Stop Loss: ATR-based above the trap candle high to avoid minor wick stops

Take Profit: 2:1 Risk-to-Reward ratio

Seller Trap / Long Entry:

Condition: low < PDL AND close > PDL AND no trade taken yet today

Entry: Long at the close of the trap candle

Stop Loss: ATR-based below the trap candle low

Take Profit: 2:1 Risk-to-Reward ratio

Only the first trap trade of the day is allowed to avoid overtrading.

d) Risk Management

Stop-Loss (SL):

ATR-based to account for market volatility

Ensures the trade survives minor wick sweeps without being stopped out prematurely

Take-Profit (TP):

Fixed 2:1 R:R relative to SL

Ensures each winning trade outweighs potential losses

Trade Frequency:

Only first trade per day is allowed, making it highly selective and reducing noise

3. Visual Features

PDH/PDL Lines: Anchored to previous day, extend into current day, color-coded:

PDH → Green

PDL → Red

Trade Labels: Placed on the trap candle:

Short → Red label “Short”

Long → Green label “Long”

The visual markers make it easy to identify exactly where the trap occurred and the trade was triggered.

4. How the Strategy Works – Step by Step

Example for Short (Buyer Trap):

Market opens, PDH/PDL from yesterday are drawn.

Price spikes above PDH → some buyers enter expecting breakout continuation.

Price immediately closes back below PDH, trapping buyers.

The strategy enters short at the close of the reversal candle.

SL: placed above the trap candle using ATR to give room

TP: calculated as 2x the risk (distance from entry to SL)

Trade executes — first trade of the day. Any further trap signals today are ignored.

Example for Long (Seller Trap):

Price drops below PDL → some sellers enter.

Price immediately closes back above PDL, trapping sellers.

Strategy enters long at the close of the reversal candle.

SL: below trap candle using ATR

TP: 2:1 R:R

Trade executes — only first trade of the day.

5. Why This Strategy Works

Exploits liquidity zones: Markets often hunt stops above PDH or below PDL.

High-probability reversals: Trapped traders create strong counter moves.

ATR SL: avoids being stopped by minor market noise or wick spikes.

Selective trading: Only first trade per day → reduces overtrading and noise.

Clear visual markers: Makes manual observation and confirmation easy.

6. Key Tips for Traders

Best on high-volume instruments like Forex majors, indices, or crypto pairs with decent liquidity.

Works well on 15m and 1H charts — 15m allows quicker signals, 1H filters noise.

Avoid trading around major news releases — traps can behave differently during high volatility events.

Always backtest and use the ATR SL — never reduce SL too much, otherwise stops will trigger before the real move.

✅ Summary:

The Liquidity Trap Strategy identifies trapped buyers/sellers using previous day highs/lows.

It uses ATR-adapted stops and 2:1 R:R TP.

Only first trade per day is executed, reducing false signals.

Anchored PDH/PDL lines and labels make trade opportunities clear.

This system is low-frequency, high-probability, focusing on trading smart rather than frequently.

PA SystemPA System - Price Action Trading System

价格行为交易系统

📊 概述 / Overview

PA System is a comprehensive price action trading indicator that combines Smart Money Concepts (SMC), market structure analysis, and multi-timeframe confirmation to identify high-probability trade setups. Designed for both manual traders and algorithmic trading systems.

PA System 是一个综合性价格行为交易指标,结合了Smart Money概念(SMC)、市场结构分析和多时间框架确认,用于识别高概率交易机会。适用于手动交易者和算法交易系统。

✨ 核心特性 / Key Features

🎯 Four-Phase Signal System / 四阶段信号系统

H1 (First Pullback) - Initial bullish retracement in uptrend

H2 (Confirmed Entry) - Breakout confirmation for long entries

L1 (First Bounce) - Initial bearish bounce in downtrend

L2 (Confirmed Entry) - Breakdown confirmation for short entries

中文说明:

H1(首次回调) - 上升趋势中的初次回撤信号

H2(确认入场) - 突破确认的做多入场点

L1(首次反弹) - 下降趋势中的初次反弹信号

L2(确认入场) - 跌破确认的做空入场点

📐 Market Structure Detection / 市场结构识别

HH (Higher High) - Uptrend confirmation / 上升趋势确认

HL (Higher Low) - Bullish pullback / 多头回调

LH (Lower High) - Bearish bounce / 空头反弹

LL (Lower Low) - Downtrend confirmation / 下降趋势确认

💎 Smart Money Concepts (SMC) / 智能资金概念

BoS (Break of Structure) - Trend continuation signal / 趋势延续信号

CHoCH (Change of Character) - Potential trend reversal / 潜在趋势反转

📈 Dynamic Trendlines / 动态趋势线

Auto-drawn support and resistance trendlines / 自动绘制支撑阻力趋势线

Real-time extension to current bar / 实时延伸至当前K线

Slope-filtered for accuracy / 斜率过滤确保准确性

🎚️ Multi-Timeframe Analysis / 多时间框架分析

Higher timeframe trend filter (default 4H) / 大周期趋势过滤(默认4小时)

Prevents counter-trend trades / 防止逆势交易

Configurable timeframe / 可配置时间周期

📊 Volume Confirmation / 成交量确认

Filters signals based on volume strength / 基于成交量强度过滤信号

20-period volume MA comparison / 与20期成交量均线对比

High-volume bars highlighted / 高成交量K线高亮显示

🎯 Risk Management Tools / 风险管理工具

Automatic SL/TP calculation and display / 自动计算并显示止损止盈

Visual stop loss and take profit lines / 可视化止损止盈线条

Risk percentage and R:R ratio display / 显示风险百分比和盈亏比

Dynamic stop loss sizing (0.3% - 1.5%) / 动态止损范围(0.3% - 1.5%)

📱 Real-Time Alerts / 实时警报

Instant notifications on H2/L2 signals / H2/L2信号即时通知

Webhook support for automation / 支持Webhook自动化

Mobile, email, and popup alerts / 手机、邮件和弹窗警报

📊 Professional Dashboard / 专业仪表盘

Real-time market state (CHANNEL/RANGE/BREAKOUT) / 实时市场状态